Financial Technology (FinTech): A Genie Out of the Bottle A brief look at FinTech in the Middle East and Europe, challenges and opportunities

Financial Technology (FinTech): A Genie Out of the Bottle

By: Bushra Nasr Kretschmer

Introduction

During my visit to Nairobi, Kenya in 2007, I was queuing at a grocery shop when I experienced an early aspect of the FinTech revolution in mobile-banking—sending money in seconds (via a Nokia 3310) outside the traditional, sophisticated, banking system. The Magic-Pesa was what I named it!

The typical infrastructure of the banking system we know is based on physical branches, lengthy bureaucratic procedures, strict ID identification processes, elite customers and elegant dress-codes for the banks’ officers, governed with tough provisions and regulatory structure based on Basel regulations. Any transaction carried out beyond the banking system comes with a stigma of being illegal while any transaction within the system is charged with different types of fees. In this way, the banking sector can exert great control over global finances.

M-PESA was one of the core innovative technology drivers for FinTech made by young Kenyan entrepreneurs. When Steven Jobs introduced the all-powerful iPhone, mobile banking sparked. Even today, innovation in mobile banking is still taking place and it is hard to imagine how this sector will look like in a decade.

M-Pesa entrepreneurs were smart stenographers of the banking system. They focused only on the core elements of banking, namely software, connectivity and agents. They replaced the limited sophisticated elite bank branches with unlimited number of agents and embedded the banking services software within the telecommunication sector. Basically, they provided banking services with no banks. Since then, we have seen technology driver start-ups which have disrupted the industry and strongly influence our lives. They sought to change the way financial services are offered to the end consumer. According to EY’s 2017 FinTech Adoption Index, one-third of consumers utilise at least two or more FinTech services and those consumers are also increasingly aware of FinTech as a part of their daily lives.

Where Does the Story Start?

The evolution of banking through the years, from the first traditional bank that was established in 1642, Banca Monte dei Paschi di Siena, to the first electronic recording for accounting in 1953, that moment onward, modern technology started to transform banking. The computerised system arrived in the 1950’s where it created general ledgers and core systems for banks. In the early 1980’s, with the creation of telephone banking and the access to the internet, all of those cases created the technological transformation of banking. However, FinTech technology now is really kicking us in high gear and drastically changing how people carry out their banking activities.

Banca Monte dei Paschi di Siena still functions. I visited the original bank twice and always wondered how Siena’s municipality and the bank preserved its structure, history, and archives despite the many conflicts and upheaval the region went through. How did the bank not fall apart and vanish into bankruptcy?

Despite the creation and development of banks, after 396 years of banking,i still an entire 1.7 billion people live their lives without availing any banking services. Meanwhile, we are starting to see how FinTech plays a pivotal role in increasing banking usage in weaker economies. Furthermore, FinTech’s role in boosting the level of consumer satisfaction is growing and has widened its complementary services to provide flexibility with low prices, an efficient and faster process. Basically, it reached the type of consumer the banking sector could never tap into.

Fintech, digital technology, are bases for starting smart cities where traditional networks and services are made more efficient using digital and telecommunication technologies for the benefit of its inhabitants and business. This 21st century digital technology revolution, its rapid acceleration and growth, is like a genie that popped out of the bottle where we are unable to anticipate where it will lead or stop. This article focuses on FinTech Technology, its opportunities, and sectors. Along with an overview on its current status, and what was the effect of COVID-19 in accelerating its development. Finally a quick overview on FinTech in the Middle East North Africa and Europe and its challenges. It concludes with recommendations for the sector.

What is FinTech?

KPMG’s 2018 figures note that global FinTech funding rose to $111.8 billion (USD) in 2018ii up 120% percent from $50.8 billion in 2017. Today FinTech is a venture industry of around $140 billion a year.

The FinTech label is very broad and there is no consensus about its definition and it may be premature to define a field that is so rapidly evolving. What is clear is that it is technology and innovation that aims to compete with traditional financial methods in the delivery of financial services. We can use the definition of Dorfleitner (et al, 2017) who argues that: “FinTech” denotes companies or representatives of companies that combine financial services with modern, innovative technologies. It is an emerging industry that uses technology to improve financial services. It offers 24/7 access to bank customers and services that are available via channels such as social media and the internet. The application programme interfaces (APIs) enable FinTech to develop value-added solutions and features that can easily be integrated with banking platforms.

Meanwhile, the FinTech industry has sustained a double-sided contribution, with innovation coming not only from new start-ups and entrepreneurs but also from within the ranks of some of the major financial players around the globe. It has solved problems with the help of latest technology and ensured it is accessible to everyone.

FinTech opportunities may be summarized as:

- Greater access to capital—This appears in the Pear to Pear (P2P) and Equity Crowd Funding (ECF) platforms in providing credit to borrowers, especially Small and Medium Enterprises (SMEs), which do not have access to bank loans and opening new possibilities of access to equity finance.

- Financial inclusion—Digital finance has improved access to financial services by under-served groups. Technology can reach remote locations.

- Better and more tailored banking services—to deliver a cost effective and flexible service via, for instance, robo-advisors to help customers navigate the investment world and create a better and tailored customer experience.iv

- Cost advantage—It provides lower transaction costs and faster banking services such as cross-border transfers.

- Fragmenting incumbent banks—decrease their systemic risk and create positive impact on financial stability due to the increased competition of new players competing with incumbent banks.

- Regulation Technology (Regtech)—Contemporary, innovative technologies, can help financial institutions comply with regulatory requirements and pursue regulatory objectives.

- Enhancement in security—as security is built into the blockchain through encryption of the blocks and linkages between the blocks. FinTech Platforms also provide various methods to ensure anonymity and prevent information leakage.

The industrial segments of FinTech include :

- Payment is the largest sector of growth in financial services. FinTech’s disruption of the sector over the past decade was a great achievement of this era of innovation; enhancing convenience and customer experience. It has also added a new layer of competition with FinTech start-ups competing in a space that has been dominated by credit card processors and financial institutions. FinTech innovation is also, in part, dependent on the blockchain innovation, which is a system that records transactions in literal blocks that form part of a chain (of transactions) resulting in a safe ledger system. The blockchain system itself is nothing short of revolutionary and its applications are found not only in the financial sector but also in many other sectors, most notably the cyber security sector.

Some of the disruptive trends taking place in the area of money and payments include:

- Mobile banking: The smartphone is already the centre of a modern consumer’s life.

- Peer-to-peer transfers: since blockchain intermediates the need for middlemen to facilitate and authorise transactions between two parties, there is a significant reduction in costs that the users are required to pay when transferring money.

- Insurance Changing consumer behaviour and advanced technologies are disrupting the insurance industry. Additionally, Insurtechs and technology start-ups continue to redefine customer experience through innovations such as risk-free underwriting, on-the-spot purchasing, activation and claims processing.

- Regtech is the management of regulatory processes within the financial industry through technology. The main functions of Regtech include regulatory monitoring, reporting, and compliance. Regtech, or RegTech, consists of a group of companies that use cloud computingvi technology through software-as-a-service (SaaS) to help businesses comply with regulations efficiently and less expensively. Regtech is also known as regulatory technology.

- Wealth Management—The emergence of robo-advisors, or the computer-automated investment platform, along with the proliferation of artificial intelligence (AI) tools, has transformed the way financial advisors interact with and provide services to their clients.

- Crypto currencies/blockchain—blockchain is the technology that underlines digital currencies—such as bitcoin. It functions as a distributed ledger that enables transactions between peers without the need for mediations by centralised, trusted third parties. Its potential functionality is immense and is not confined to financial services. Although bitcoin is the best-known digital currency, there are various others in existence and in development. While cryptocurrency itself has endured an erratic history, the allure of virtual money continues to be its underlying technology and the future products and services that could be built on top of this foundation.

- Cyber security—As the FinTech sector grows, so does the need for up-to-date cybersecurity. As the number of connected devices continues to rise steeply, financial technology becomes cheaper and easier to use. Processes and services which were once monopolised by banks are now much more accessible to companies and the wider public. This has the added benefit of increasing innovation, lowering operating costs and improving the efficiency of financial institutions. However, whether it be social security numbers, payment card numbers, PINs and passwords, financial information remains sensitive and must be protected. Currently, the banking sector does a decent job of protecting people’s data. The most pronounced challenge for FinTech is to prove that it provides at the very least a similar security level. If there is any lapse in this area, people will start distrusting applications and want to revert to traditional banking.

The FinTech ecosystem has stimulated technological innovation, made financial markets and systems more efficient and improved the overall customer experience. It is composed of five main elements:

- The governments, embodying the regulations and legislations

- The financial institutions, traditional banks, stock market, insurance companies, venture capital

- Start-ups and entrepreneurs, representing the payment systems, wealth management, crowdfunding, insurance FinTech, etc

- Technology Developers, cloud computing, Big Data Analytics, cryptocurrency, social media developers, etc

- Business environment/access to markets representing the financial customers, individuals and companies

The quality of infrastructure is critically important. This includes the state of physical infrastructure, the ecosystem’s connections such as distance to existing business hubs and ease of access), the utilities (power, water, telecommunication, etc.) and the overall quality of real estate and facilities. Governments can influence many aspects of the ecosystem, including easing business regulations such as copyright.

The FinTech regulator covers land and real estate, equipment, technologies, and utilities. Another factor is the degree of integration and synergies among the players involved. Technology clusters or hubs, where entrepreneurs have similar business objectives and are integrated, make it easier for the ecosystem to flourish. These clusters promote the availability of skilled labour (such as banking analysts, IT developers, sales force, and management staff).

FinTech ecosystems are typically funded through four main sources. Governments may fund the construction of the FinTech hub by providing seed funds, interest-free grants, or even through provision of subsidised office and co-working spaces. This can be done with banks in a consortium. The government may also provide initial financial support to venture capital or private equity funds, banks, and incubators to encourage investment in small businesses. Venture capital funds and private equity shops are traditional investors in FinTech start-ups. Funds ’involvement will typically increase as these business models gain momentum. Incubators and accelerators prepare businesses for venture capital fundraising and provide grants and investments. By offering financial and due diligence services to entrepreneurs, they become a one-stop shop for buyers and sellers in the ecosystem.

Broad financial expertise and know-how is necessary to structure the ownership of a FinTech ecosystem, provide advisory services to entrepreneurs from the early stages of idea generation through commercialisation and provide legal and regulatory counselling to ensure adherence to local law and tax regulations. These experts can also be instrumental in lobbying for financial or regulatory measures.

Impact of COVID-19 and Accelerating FinTech

Shedding light on the post-financial crisis of 2008, changes started taking place in the financial industry in terms of its societal impact. The Covid-19 crisis has both reinforced and fast-tracked these changes. The pandemic has drawn attention to the fact that capitalism really was not about solving problems such well-served public health service, income inequality and climate change that we see emerging. The industry works as a reaction to capitalism and it has lost sight over its social license and social responsibility.

Technology is driving this change and is shaping a different future across all players for social and financial inclusion. The rise of techno socialism has produced highly automated societies. There is a need to create more social consciousness within capitalism. If we had a social consciousness, we would not have problems with climate change—for instance.

Another positive outcome of the Covid-19 crisis is that it has caused an increased focus on cashless payments and digital identification. Fiat money became a sanitation nightmare while FinTech focused on offering digital banking solutions is likely to see a positive boost.

The consumer increase in the use of mobile devices encouraged financial institutions to partner with FinTech providers in order to keep up with the pace of innovation in the financial sector. We saw more deliberate efforts by the FinTech companies to serve the communities in

partnership with regulators, central banks and policy makers. The broader push during digitalizsation embraced FinTech and expanded capital distribution to consumers and SMEs. The Challenger Bank N26 for instance, reached six million customers across Europe and the US. And the money transfer operator for remittances Enjaz Saudi Arabia achieved 27% accounts opened remotely without visiting their branches.vii Additionally, in an attempt to boost the economy, the policy makers and regulators are looking for ways to ease regulations on FinTech companies, which would stimulate growth and expansion in that sector. E-commerce giants have expanded their goods and services at lower costs and FinTech is responsible: it helps reduce the cost of finance and opening up the markets, optimising process efficiency and improving security. Industry silos are merging and partnerships between financial institutions, biotech platforms, FinTech startups, scale-ups that leverage the best of balance sheet, products, user engagement and technology are increasing as they build something that is more powerful than the sum of its parts.

The Main Challenge in FinTech is Regulation

Technologists today are very advanced — specialising in areas that are generally under-appreciated by traditional banks — and use digitalisation to make processes easier for customers. Most of the major challenger banks were founded in the past five years and they tend to be characterised by mobile first apps, personalisation and customer centricity. However, the technology regulator is not up to speed with these innovations and it is essential to reinforce the banking sector to adopt and build around these technologies such as personalisation in terms of security, documentation and facial recognition, which is all delayed due to the regulatory approval. In this way, regulation is becoming a hurdle in improving the banking sector and getting it up to speed with the latest developments. Enhancing the efficiency of building, enabling, and adopting the eco-system of FinTech mainly the regulatory framework is a must. Only in this way can real development and innovation start to translate into the practical lives of the people using the system.

Financial services are among the most heavily regulated sectors in the world. As these financial regulations protect consumers’ investments, prevent financial fraud and limit the risks financial institutions can take with their investor’s money. Regulators oversee three main financial sectors: banking, financial markets, and consumers. FinTech regulation is the chief concern among governments as FinTech companies take off. Most of the regulatory environment governing most banks is mainly about the stability of the financial system rather than the competition and innovation within.

To what extent the regulatory environment is supporting innovation and competition and to what extent is the regulatory environment supervise these activities in a safe environment without jeopardising any risky implications are crucial questions. The role of the regulators needs to be clearly defined so they can carry out their duties without issue. If regulators know the scope of their work, the rest of the community can also improve knowing in advance how to work in a way that results in the fastest approval of their products and reduces hurdles. It is extremely important to keep in mind that the benefit from FinTech should not be at the expense of safety and soundness of the financial sector or consumer protection.

The Basel Committee on Banking Supervision in 2017 stated that the Banking standards and expectations should be sufficiently flexible to accommodate new innovations within the appropriate statutory authorities of jurisdictions; nonetheless, the high standards for safety and soundness and consumer protection objectives required in the banking industry need to be maintained. Tight regulations can kill the FinTech industry and innovation. The regulator should work as an enabler for emerging FinTech startups—not as an enforcer, trapping them with traditional regulations, bureaucratic organisations or banks.

As these traditional organisations and regulations will kill innovation. To avoid this, the regulator should move fast to catch up with the FinTech and consumer experience. Otherwise consumer experience is so far ahead of the infrastructure and regulation that it could cause a breakout in the system.The role of the innovation ecosystem that works outside of traditional organisations and interacts with evolving civil service environment should be encouraged and supported. The regulator can enable evolution within the financial industry or hinder evolution in the market. For instance, the Nordic countries are making considerable progress in the transition towards cashless societies and Sweden tops the list while regulations and infrastructure rest at the heart of the problem in the Middle East.

In the US and Europe, the FinTech ecosystems have stimulated technological innovation, made financial markets and systems more efficient and improved the overall customer experience. And, the government’s role is limited to policy setting, regulations and property development and the private sector dominates the services scene.

In less-mature FinTech environments, such as Jordan or Saudi Arabia, the government is involved across the entire ecosystem. Another way of easing the regulatory framework is to break down regulatory elements. A good model to view at is Singapore’s FinTech sector as the government encouraged financial innovation and mitigated risks brought by FinTech through institutional improvements and regulatory reforms.

It also identified potential regulatory limitations and highlights the methods through which these can be handled:

1. they reformed the regulatory authorities to encourage financial innovation (re: the introduction of the FinTech Regulatory Sandbox and its improvement)

2. improved the integration of regulatory infrastructure by establishing the Monitory Authority of Singapore (MAS) FinTech & Innovation Group

3. issued regulatory guidelines and passing laws to provide regulatory clarity in response to the evolving FinTech sector by the issuance of the Digital Token Guide. reformed laws such as enhancing of the Payment Services Act.

Singapore’s experience could provide useful insight to regulators that are endeavouring to promote the formation and growth of their FinTech sectors.New payment infrastructure, in partnership with large tech platforms, to distribute across their massive and highly engaged user-base, leveraging payment network and liquidity while plugging in new FinTech players to optimize payment process or digital identity verification and FinTech like thought machine.

The FinTech industry needs to sustain and build on such collaboration and interoperability and provide help where it is needed for their customers and the wider economy. The industry needs to change its business model, the deployed technologies and the operating procedures.

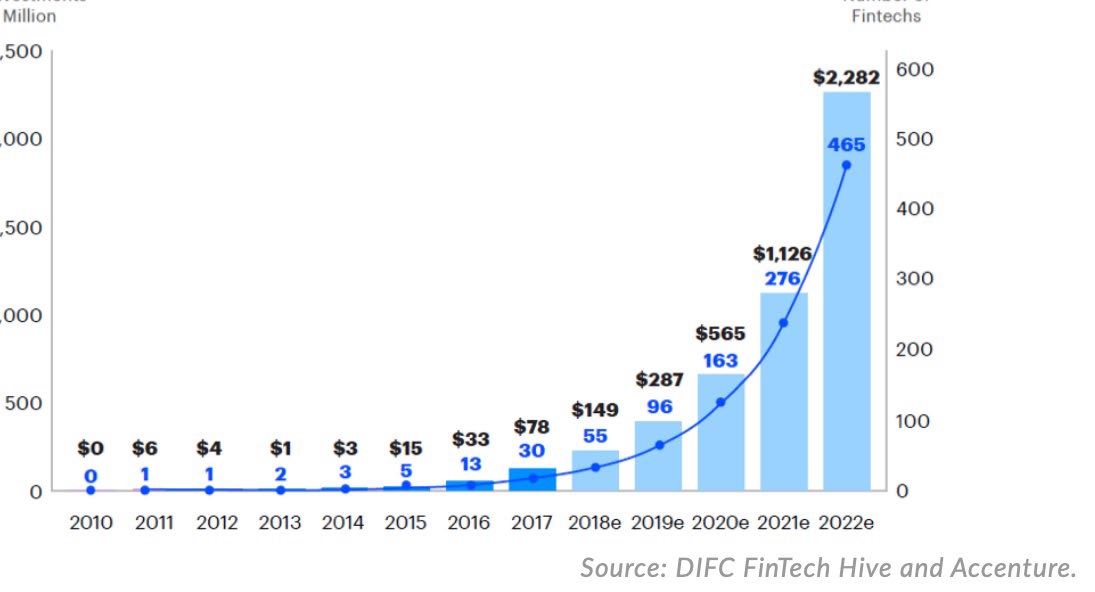

A Quick Glance at FinTech in the Middle East and Europe

In the Gulf region, policymakers and regulators began implementing forward-thinking and agile policies related to FinTech beginning in 2017x. Since then, significant energy has gone into designing more diverse, competitive and innovative economies and the financial sector plays a key role in the massive effort to shift Gulf economies away from the heavy reliance on government spending and the energy sector. FinTech is booming in the Middle East and North Africa (MENA), representing one of the hottest industries in the region, according to a new report by investment data platform Magnitt and the Abu Dhabi Global Market (ADGM) international financial center.

In Bahrain: the financial sector is one of the most important non-oil sectors in the Kingdom’s economy, which accounts for over 17% of the Kingdom’s gross domestic product (GDP)xi. It launched Fintech Bay back in February 2018xii and it provides a physical hub to incubate insightful, scalable, and impactful fintech initiatives through innovation labs, acceleration programmes, curated activities, educational opportunities and collaborative platforms.

In Saudi Arabia, the venture capital financing increased remarkably by 55% in 2020, reaching a record high of $ 152 million despite covid19. Financing for start-ups in Saudi Arabia grew faster than the average in the MENA region: 17 countries in the region saw a 13% increase in total funding from 2019 to 2020, Saudi Arabia saw a 35% increasexiii.

In the United Arab Emirates (UAE) is a great example where incubators, enterprise development funds and programmes, and innovation hubs are supporting the creation and growth of local entrepreneurs.

The FinTech ecosystem is seen as a leading pillar of economic diversification across member states of the Gulf Cooperation Council. GCC countries have not established a particularly good FinTech ecosystem despite the existence of the main ecosystem in the area. Amazingly, there

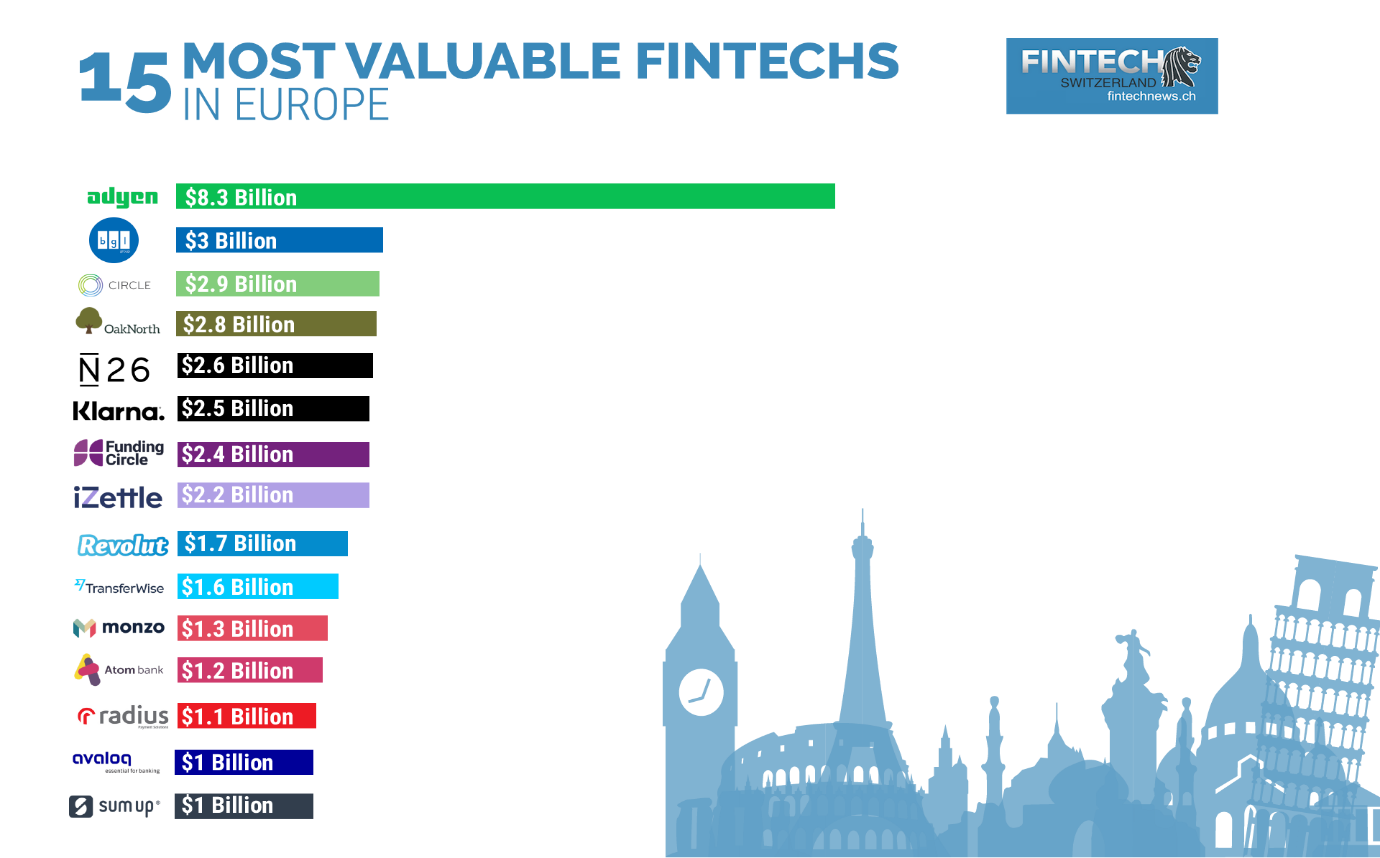

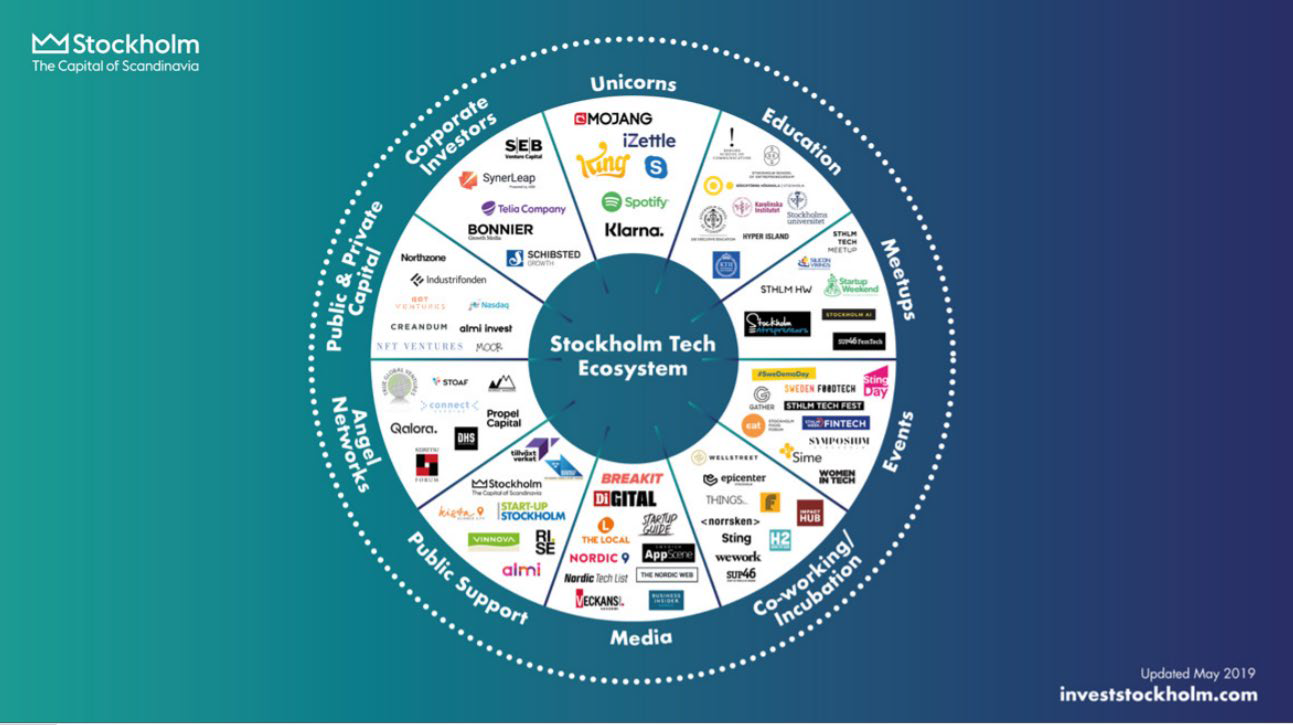

are success stories in the Gulf Countries, however, what is missing is enabling and deepening the innovation FinTech ecosystem and enabling the integration and synergies among the players as it is in Europe illustrated as example of Sweden FinTech ecosystem in figure above. The FinTech ecosystem is not about matching promising ideas to financing, it is about generating innovative ideas through the interplay elements of the FinTech ecosystem and the involvement of multiple stakeholders, including the media, disruptive non-bank players, universities, software and infrastructure providers, and venture capitalists.

Technology clusters (or hubs), where entrepreneurs have similar business objectives and are integrated, make it easier for the ecosystem to flourish. These clusters promote the availability of skilled labor (such as banking analysts, IT developers, sales force, and management staff). In the meantime, the Government/regulatory support can influence many aspects of the ecosystem, including easing business regulations (such as copyright, product registration, initial public offering [IPO] requirements) and keeping taxes and fees low. However, the extent of the government’s involvement can vary. In mature FinTech countries, the government’s role is limited to policy setting, regulations and property development.

Last word

The international financial system bears witness to the rapid development and innovation-fueled approach to problem-solving. The FinTech Community is taking over traditional banks and an inclusive, greatly democratized banking industry taking over the incumbent institutions in the sector. Many challenges remain but the industry ensures that the disruption does not affect consumer protection and financial stability. Policy makers should engage in greater focused investments and should rethink their responsibilities as regulators. Focus on the simplicity not the complicity to accelerate innovation and transformation that creates genuine results.

End Notes:

- i https://sv.wikipedia.org/wiki/Banca_Monte_dei_Paschi_di_Siena

- ii Lauren M. Mostowyk, “Regulating FinTech: The Case of Singapore”, Aug,2019.

- iii Peters & Panayi,” According to the global specialized reports and studies” (BCBS, 2017; Financial Stability Board, 2017; IOSCO, 2017), 2016)

- iv A robo-advisory is a digital platform that provide automated, algorithm-driven financial planning services with little to no human supervision.

- v Ahmed Taha Al Ajlouni, and Monir Suliaman Al – Hakim, “Financial Technology in Banking Industry:

- Challenges and Opportunities”, February 2019.

- vi Cloud computing is the delivery of different services through the Internet. These resources include tools and applications like data storage, servers, databases, networking, and software.

- vii Challengers specialise in areas that are generally underserved by these bigger banks, using digitalisation to make processes easier and simpler for customers. Most of the major challenger banks were founded in the past five years. They are characterised by mobile first apps, personalisation, and customer centricity

- viii KPMG, “The Pulse of FinTech, HI 2020”, September 2020.

- ix Thought machines comes in as many banks have the ambition to deliver better technology to their customers but are held back by legacy platforms and technology. Cost of change is huge, and cost of operations is too expensive because of an inability to automate processes.

- x Jackson Muller, and Michael S. Piwowar , Milken Institute. “The Rise of FinTech in the Middle East”, 2019.

- xi The Fintech Times, In-Depth Analysis: The Fintech and Financial Services Economy of Bahrain, September 12, 2020.

- xii https://www.bahrainfintechbay.com/press-release.

- xiii Magnitt Report, Venture capitalization in Saudi Arabia in 2020 report, 2020.